My first post! I haven’t yet set a standard template for company analysis, but I intend to do so to help keep things organized. I will also include charts to help convey what I am evaluating. I plan on starting my blog by reviewing my holdings in a series of posts.

Overview

I’ve held CNR since July 2015. It’s done fairly well for me in terms of dividend growth (11.7% CAGR) but less stellar in terms of share price appreciation (approx 7.6% CAGR). I’m now trying to view my investments with a value lens and with news of a strike on the horizon earlier this year, I thought it might be a buying opportunity. Shares have come off the their earlier highs of ~$178/sh to trade around $155/sh, down about 15%. I like CNR as a company with its wide moat – those railroads aren’t going to be replicated – and decent operating returns (+/- 15% ROIC) and, in my view, a safe dividend payer (FCF dividend payout around 50-60%). I almost added to my position this year with that view in mind but tried to put a valuation lens on it and passed. My conclusion is that I don’t think the share price is low enough .

In the short-term, while I’m worried about the strike of course, I don’t think it will be a drawn out issue considering the significant of labour disruption on the supply chain. There may even be legislative solutions implemented when the Feds return to the Fall session, if it comes to it. I won’t ruminate on what might happen if the strike runs a long time. In itself, it was already a known factor. This is how I came to my conclusion and decided to pass on adding more at the moment.

Setting the Context

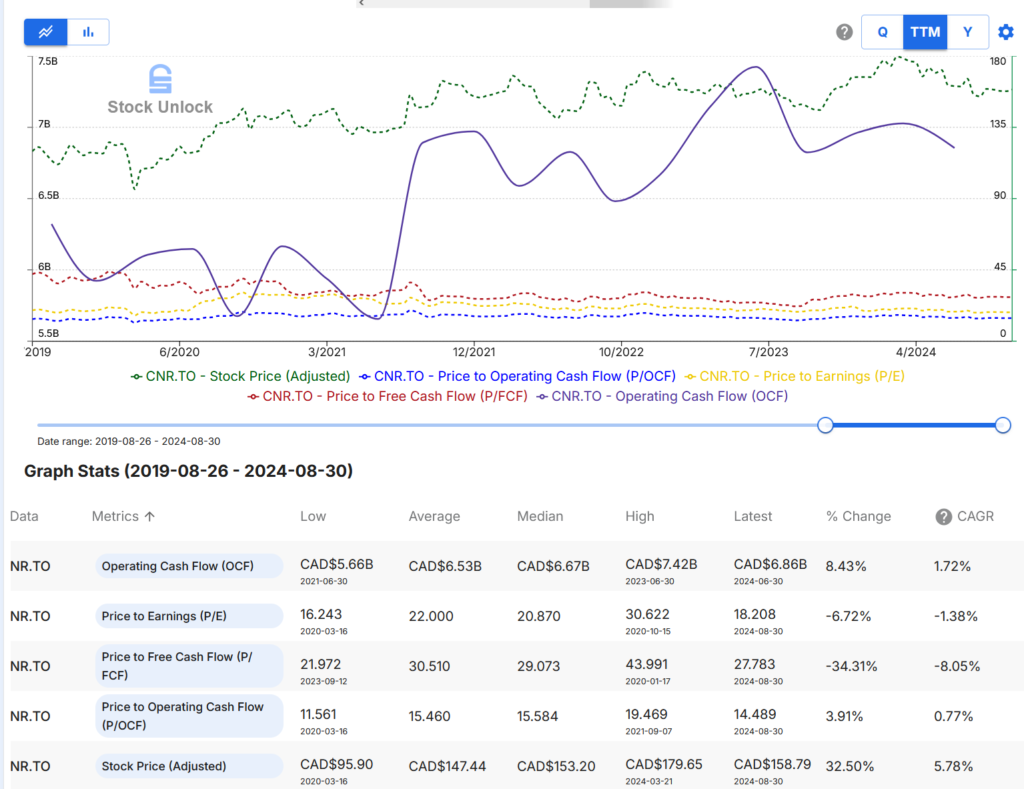

What I saw was that the share price run up in 2024 came mainly from multiple expansion (both P/E, P/OCF). The underlying performance was pretty stable; $6.8-7B OCF and $5-5.5B earnings. I’m giving a range because I’m scanning TTM metrics over a few quarters.

Going back 5 years, the CAGR is about 4% for earnings and 2% for OCF. Neither are stellar, but shouldn’t be surprising, because it’s a railroad that is the backbone of the economy, not a tech growth stock.

As of late August, both multiples are sitting around the median: 18x actual PE vs. 20.7x median and 14.3x actual P/OCF vs. 15.5x median. Yes, perhaps a little cheap by historical standards but not much of a discount.

Stock Unlock: Free Form tool for CNR

This is a good candidate to value based on FCF since its fairly steady despite $2.5-4B of investments per year. The story is the same in terms where the multiples sit. In the past 5 years FCF has grown at a good clip of 12% p.a., but stock price has only moved at ~4% CAGR, so P/FCF has shrunk by 6% p.a. (!!). Maybe there is an argument for multiple expansion? The 27.5x P/FCF multiple is a bit below 30x median and still high off the 22x low from last year. Unfortunately, FCF itself is also trending down, due to a double whammy of higher capex and lower OCF.

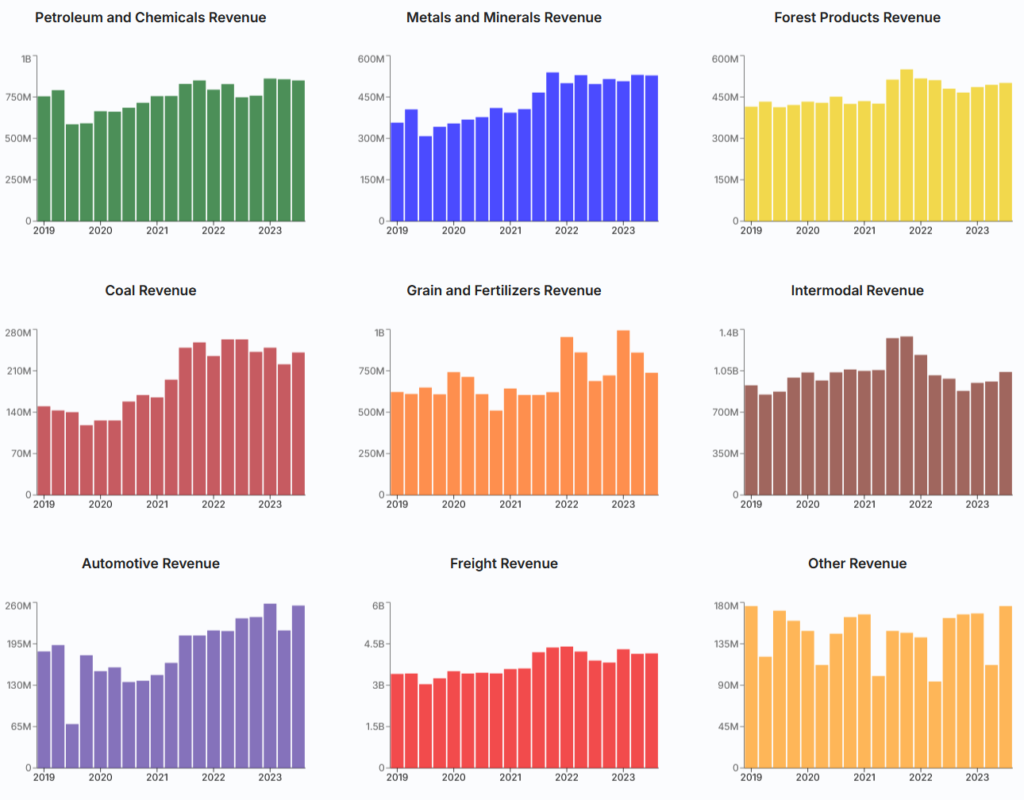

A lot of their cargo is commodity based and at the moment, on a quarterly basis it seems to have flatlined (pet chems, metals/minerals, grain and fertilizers, coal, freight and automotive). Some very slight growth in intermodal and forest products:+

Stock Unlock: KPI for CNR as of 2Q24 (pulled Aug’24).

I don’t see the underlying part of the multiples growing at the moment. Especially not with my concerns over the consumer. By which I mean too much mortgage, car and credit card debt that will dampen demand now that excess Covid-era savings have been used up. Industrial activity is fairly anemic too, according to declining Purchasing Manager Indices in both Canada and US; I still think the IRA in the US will provide a secular tailwind but at the moment the investment isn’t yet happening in a big way. CNR even mentioned on their July Q2 earnings call both softness domestically and oversupply of truck capacity leading to lower revenue per track mile, with further expected challenges due to the then-anticipated strike.

Valuation

Using the DCF calculator on Stock Unlock, and if I merely assume historic performance over the next 5 years (growth and average price ratios), we get 8% CAGR and a FV of ~$145/sh on a OCF basis and almost 13% CAGR on an earnings basis with a FV of ~$178/sh. If we believe guidance of mid-to-high single digit earnings growth, say 7.5%, then share price CAGR is nearly 16%…if they can sustain that for the next 5 years and P/E ratio expands back to the 5 year average of 21.9x from 18x currently.

Then it starts to look really attractive on a FCF basis assuming historic growth rates, with a FV of almost $230/sh and nearly 19% CAGR. I don’t believe it, though. Capex has run up about 6% p.a. since the Pandemic and see my comments above about demand. Multiples also have to expand, and recently, OCF has tumbled a bit. Part of the longer historic price run up was the company’s move to precision based railroading (PBR), and more recently since 2020/Pandemic, pent up demand driving volumes and helping push up all results.

Arguably CNR moved away from the intensity of PBR in recent years and could do a bit more to eke out better margins, driving up OCF and earnings, but I don’t think there is a lot of excess cost to trim without sacrificing operations and safety. Searching online already reveals many news articles about those issues; indeed that’s part of what the strike is about.

Concluding Remarks / Actions

CNR doesn’t fit my value-objective at these prices because I don’t think it’s compellingly cheap. Reasonably priced? Yes, probably, but not market beating. Conversely, I don’t think it’s significantly overpriced so I won’t sell my main holding for now. I have a small position in a side account and will swap that for BN.