Thermo Fisher Scientific (TMO) provides serves the healthcare industry, specifically providing a range of analytical instruments, equipment, reagents and consumables, software and services. Formed through the merger of Thermo Electron and Fisher Scientific in 2006, and operating in over 50 countries. Their market cap is over $200B as of writing. In late 2024 I swapped my holding in JNJ for TMO. This serves to summarize my thinking about TMO.

They operate four segments with leading positions in each:

Customers

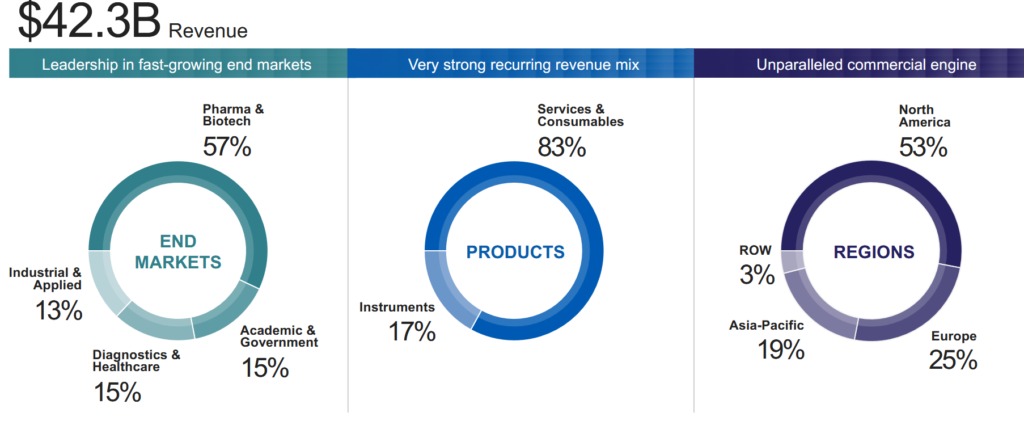

Customers include pharma, biotech, hospitals, clinical diagnostic labs, universities and research institutions. I would describe TMO’s products as the ‘picks and shovels’ for healthcare.

Customers are diverse by geography and industry, with a notable, and expected, concentration in pharma & biotech:

Customer retention rates are high due to the mission-critical nature of products, long-term relationships often spanning decades, recurring revenue from consumables and services, integration in customers’ processes, and comprehensive post-sale support. After selling the equipment (17% of revenue), customers need the material to operate them on an ongoing basis, and will buy the consumables and services from TMO (83% of revenue). It’s simple to go to a single provider.

They prioritize customers and have “experience centres” to support them, e.g. New centre opened in Korea to support material sciences, specifically battery manufacturers. I like this additional business outside of healthcare.

Competition

Competitors include Agilent technologies, Waters Corp and Danaher in Life Sciences. Of these, only the last provides any sizeable threat with ~$170B market cap compared to TMO’s ~$200B. Over the past decade TMO has been able to:

- Grow its FCF at a CAGR of nearly 14% (currently $7.8B for Q3/24 LTM vs. $5B for Danaher).

- Grow EPS at a 13% CAGR vs. DHR’s 4%.

Competitors for diagnostics include Roche, Siemens Health and Abbott; and in Laboratory these include Merck, Sartorius and Eppendorf. No one perfectly lines up against TMO in terms of product offering, and for many EPS growth is on a similarly low trajectory as compared to TMO. I also prefer not having pharma exposure.

I was able to quickly comp competitors’ performance, easily from Stock Unlock’s Free Form Tool (unaffiliated link). For example, the valuation:

Operations

TMO is an acquisition machine, which has been its growth engine in the past decade-and-a-half. Since 2010 they spent nearly $5B p.a. buying other companies. This was fuelled by cheap debt, which may become challenging where rates are now. Also, given its large size, additional acquisitions have a diminishing impact on growth.

It is a fragmented industry, however, and TMO has proven itself able to execute on M&A, consistently. Their largest acquisition recently was the $20B purchase of PPD in 2021. It is performing well, with new customer wins, increased customer retention and share of wallet, and synergy targets raised in 2023 now on track to exceed $200MM in operating income by year 3.

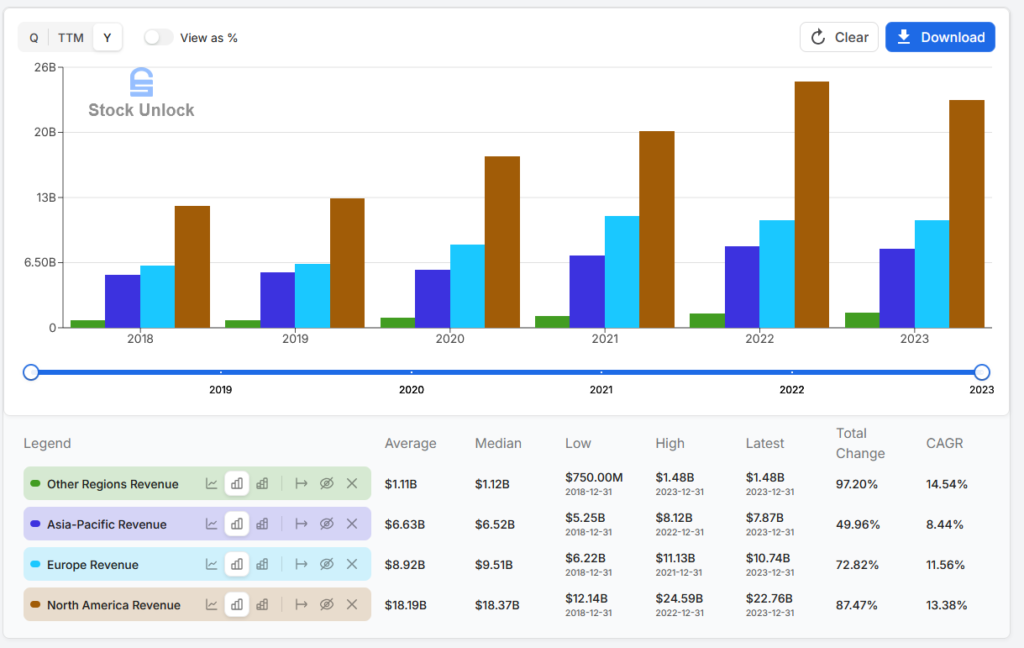

China is not an insignificant contributor to results, so slowing growth may be a concern but it is not the only country in Asia that TMO serves, nor is it the largest segment. The base is firmly North American:

Stock Unlock: Financials and KPIs for TMO

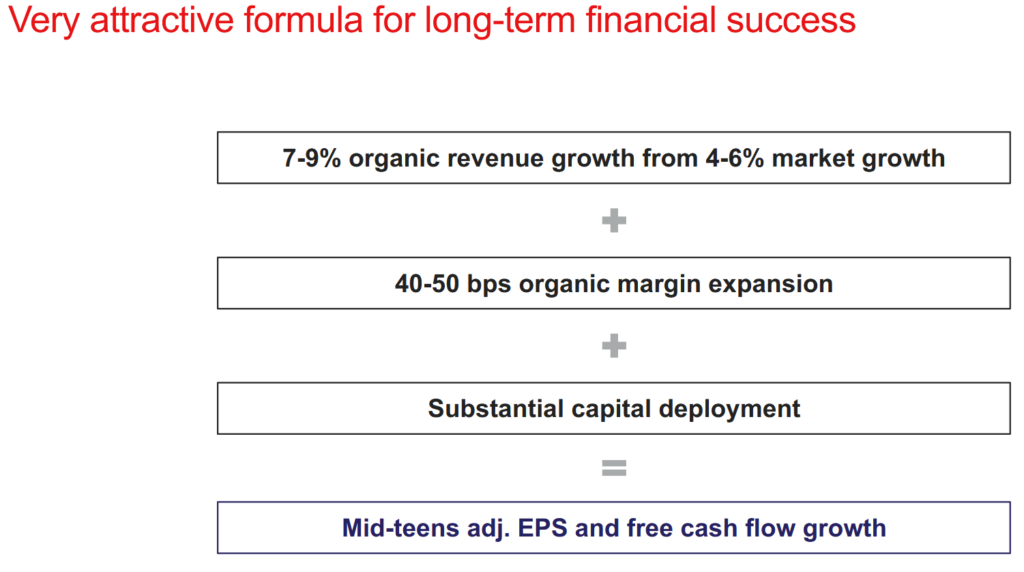

TMO claims to serve a $235B market with 4-6% long-term growth. End markets benefit from enduring long-term trends including:

- Favourable demographics driving up demand for healthcare (aging)

- Global population growth (by 2035, 1.2B will be >65 years old, +50% from 2023)

- Ongoing advances in life sciences research

- Funding momentum in pharma and biotech

- Development of complex therapeutic modalities and customized patient demands

- Material science breakthroughs growing semiconductors, advanced materials and energy transition

Financial Review

They focus on several pillars:

- Innovation

- Leveraging scale

- Creating value for customers

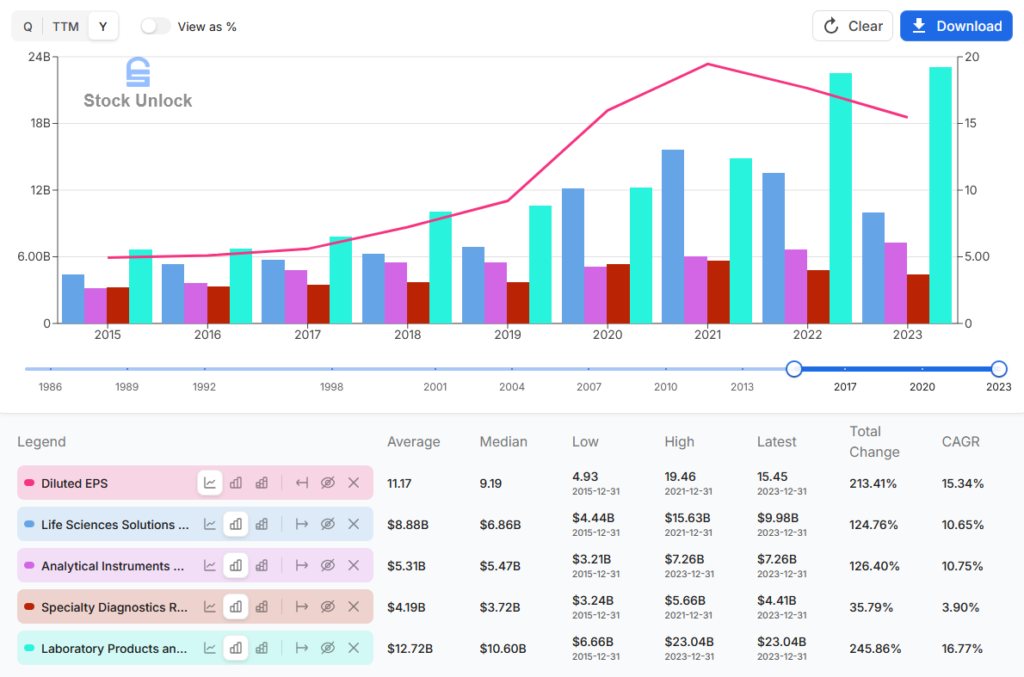

One can see they’ve benefitted from the Pandemic, which was a boon to several segments, in particular the life sciences segment. This is flagging now that we’re several years on, but this is a small segment. It’s also been more than made up for since 2022 with the $17B acquisition of PPD, in the Lab Products segment:

Just as well its the smallest segment because it has the lowest operating margins in the mid-teens. Other segments are mid/high 20%, except life sciences which is mid-30%.

They’ve reported three quarters through 2024, and so far revenue stabilized around $42B on an LTM basis. They modestly raised the low end of EPS guidance, bought back $3B of shares and continued to complete acquisitions, using cash on hand. They also launched new specialized products.

The balance sheet is in good shape, with over $6B of cash and investments and $35B of long-term debt, and an A- credit rating.

Capital Allocation

I like the focus on EPS, FCF and per share metrics. Focus is on high-ROI organic opportunities, with M&A being the primary focus of capital deployment for 60-75% of capital. The remaining 25-40% would be returned via a modest dividend and buybacks.

Share buybacks are the primary means of returning capital. Indeed, In Q4/24 TMO bought $1B in stock under its then-recently authorized program of $4B, leaving another $3B available. Since 2015 it’s averaged $1.3B in buybacks annually, with nearly $12B+ bought back since 2020. Diluted share count is down from 403MM at the beginning of 2020 to 384MM as of Q3/24 (-5% total / -1% CAGR)

A small dividend is paid (0.3% yield as of writing), which has grown at 10%+ over the past 10 years. Investors are guided that it will increase consistently over time. It represents <10% of FCF. Given the source of returns comes from business growth, I’m fine with this capital allocation.

Valuation

Setting context for their trading multiples, when I first started looking at TMO last year, I felt it was trading at a fairly rich level of almost 38x earnings and 30x FCF. That was higher than the average over the past 10 years, which were around 32x and 27x, respectively.

It’s expensive on a P/E basis but roughly in line on a P/FCF basis when only looking back 5 years, but I think the Pandemic years are skewing that (avg 5yr P/E 33x and P/FCF 31x). I think it should trade somewhere between the shorter and long term averages, because it’s strikes me as a better positioned company now than it was since the pandemic.

Source: 2024 investor day presentation

They bought back ~1.5% of their shares in the past year, and a similar amount the year prior. Assuming they continue to buy back ~1% of shares annually, dividends grow at 10% per year (lower than historic rates, but they pay so little it doesn’t really affect valuation), applying a more reasonable historic P/E multiple of 30 and a 10% discount rate, I get a fair value of ~$508/sh with 10% EPS growth for a 3yr CAGR return of 7% CAGR. If earnings grow 15% per year, FV rises to ~$580 and returns improve to 11.5%.

If I do this on a FCF basis, they’ve been able to grow it by 10% over the long-term and guiding to continuing to do that. Again, I’m trying to back out any temporal boon from the pandemic. I don’t see why that couldn’t be possible, but assumed it would grow at a 8% CAGR. This would be $9.8B by the end of 2027 which is only ~$1.7B more than the pandemic peak, and still at a much lower growth trajectory than we’ve seen in the past 2 years. Using a P/FCF multiple of 29x, in between the short- and long-term averages I mentioned, I get a FV around $588/sh at a 10% discount, for a 3yr CAGR return of 12%.

Conclusion

I think TMO presents a compelling investment case based on its dominant market position, strong recurring revenue model, and proven M&A execution. While currently trading at a premium to historical multiples, the company’s consistent growth profile, robust cash flow generation, and exposure to secular growth trends in healthcare and life sciences support the valuation.

Key monitoring points include interest rate impacts on future M&A capacity, geographic expansion success, and maintaining margins amid competitive pressures. I swapped my holdings in JNJ for TMO around $530/sh.

The combination of mid-teens FCF growth, strategic acquisitions, and shareholder returns through buybacks suggests potential for 10-12% annual returns over a medium-term horizon with a margin of safety against my estimates valuation.