Introduction

CIBC’s journey from Wall Street wannabe to steady Canadian banking powerhouse is a tale of redemption—and right now, it’s a story of success trading at a premium price. After climbing out of some of the most spectacular financial mishaps in Canadian banking history, the bank has transformed itself. But does its current stock price reflect potential or overvaluation?

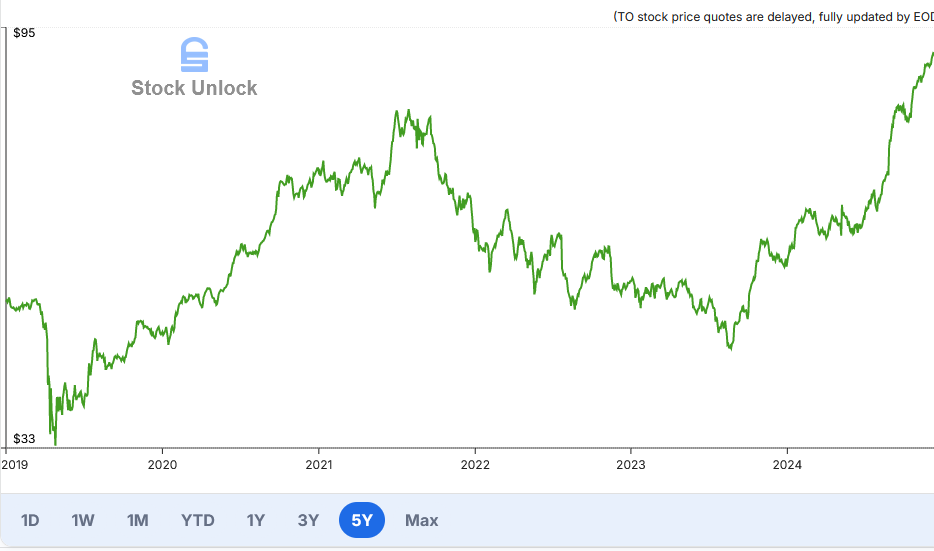

It’s been one hell of a good year for CIBC shareholders. As with all Canadian banks, their fiscal year end is October 31*, and results for Q4 and full year 2024 were reported on December 5. This one is one of my biggest positions, from my time when I was particularly focused on dividends. It’s been a good year, and purchases made during the Pandemic period have also panned out quite nicely – see this 5 year stock chart:

Before diving into this year’s results, a brief recap of their history.

Let me see your bulge…bracket

They are Canada’s 5th largest bank by assets and most domestically weighted of the ‘big 5’ notable for its very large residential mortgage portfolio. This wasn’t always the case.

They’ve come a long way since the heady days of the late 1990s and early 2000s, when then-management tried to make it a US Bulge Bracket Bank, competing with the Wall Street firms (i.e. Goldman Sachs, Morgan Stanley, JP Morgan). CIBC was involved in tech IPOs, private equity and arguably tried to be too many things to too many people. There were offices across Europe; they owned investment bank Oppenheimer; executives made the news for buying expensive real estate; CEO succession was fraught and made front page news.

Then the tech bubble popped; the bank was one of many involved in Enron and had one of the largest fines for its role (which still haunted the bank through 2019, having fought with tax authorities about how much of the expense could be deducted against income); the great financial crisis hit, and out went the share price with over $9B in subprime write downs. Leading into that CEO Gerry McCaughey had been appointed around 2005 to stabilize the good ship CIBC, and by 2008-09 many current senior executives had joined at that time from outside the bank, including Merrill Lynch, National Bank, and elsewhere.

As a result of a decade of knocks through 2010, the bank retreated to the foundation that was its Canadian business. Oppenheimer was sold; foreign offices closed or scaled back; and new business was kept to fairly vanilla banking activity. The stock was arguably overlooked by the investing community, and with good reason, having gained a reputation as the bank most likely to step onto a sharp object. That and CEO McCaughey was tasked with keeping things stable, not grow!

This meant the stock traded with a below market PE ratio. See the blue line in the chart below:

Stock Unlock: Free Form Tool, comparing the Big 5 Canadian banks’ PE in the past 10 years.

How does a company work out of a situation like this? Ideally, change the culture and prove it to investors with steadily improving results.

Show me the money!

With McCaughey retiring in 2014 – and how it came about was somewhat emblematic of old CIBC, having renewed his employment contract for three years and then deciding to depart, resulting in a very large payout – succession was brought back to the fore and there were concerns in some corners that the market would see a succession battle like times of old. Somewhat surprisingly, it didn’t happen. Victor Dodig, then head of wealth was appointed by the Board after a search.

In fairly short order, he completed a big round of musical chairs in senior executive ranks. Why? He wanted to ensure that the bank did not find itself in the situation it did when he was appointed. Specifically, he wanted to make sure that there was a “deep bench” of talent that were experts in more areas than a single business line they may have come through. Over his 10 year tenure, this shuffle in the ranks every few years continues, and it seems like results in the business are paying off.

But that skips over the rumbling that started growing a few years into Dodig’s time as CEO. He wasn’t really doing anything. What would be his legacy? What’s the bank’s story? What is CIBC, other than merely Canadian bank? It had been nearly a decade without much to speak of except the problems were past. The other banks can quickly be described – TD and BMO are very American (in different regions); RBC has global aspirations; Scotia is very big in South America.

So what’s a CEO to do? Buy something!

The Purchase of the (21st) century

In 2017, CIBC completed its record setting purchase of US bank the PrivateBank, based in Chicago. It was known for its customer focused, relationship centric lending practice in the US midwest. The purchase was initially panned after CIBC chased its prize, increasing the purchase price by 20%, in the face of reforms from then-President Trump that resulted in bank asset prices rising.

It was a bold move, that quickly started to pay off, by diversifying the bank, giving it a footprint in the US again outside of capital markets activities and a source of business deposits. Since the acquisition, the bank increased earnings from the US from about 5% at the time of the purchase to over 20% this past fiscal year.

Back to the future! Oh, and Fiscal 2024.

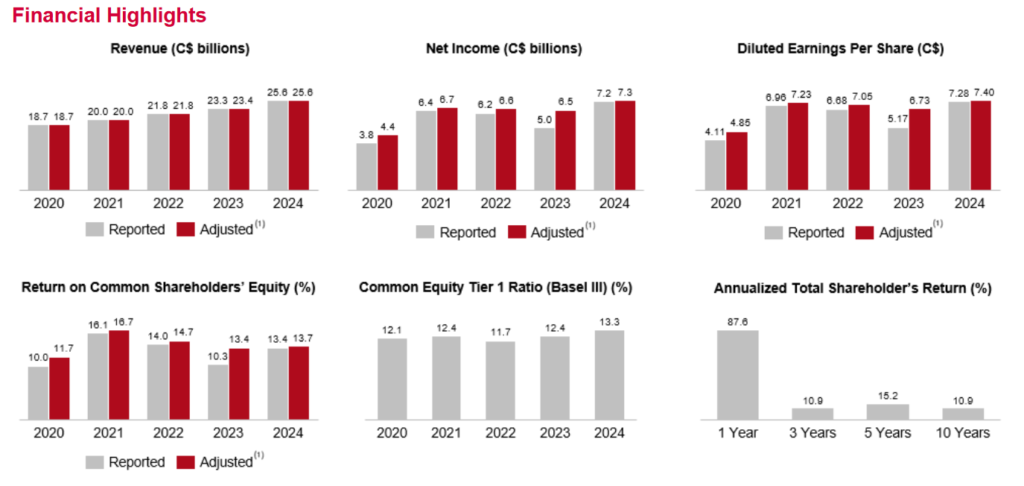

With that brief trip through time, we come back to results this past fiscal year. Handily, their investor fact sheet does the talking quite nicely, so no fancy Stock Unlock charts for this section.

Growth in most metrics have been on a steady uptrend since the 2020 Pandemic year, with some fluctuations owing to losses, particularly in the commercial office portfolio and a ~$1B provision to settle a lawsuit filed by Cerberus in 2015, which hit 2023 results (article). ROE, the common measure of returns for banks, is on an uptrend again after last year, and capital levels are well above OSFI regulated minimums.

Ironically, the Cerberus settlement plus the US regional banking crisis plus US commercial real estate concerns meant market expectations at the end of Fiscal 2023 – a year ago – were pretty low, with some worried it might signal a return to the bank of old and thus didn’t believe the emerging track record of steady results.

In other words, and perhaps with a little benefit of hindsight, the market had over-punished the stock, so with steady and quite positive results in 2024, the potential returns were quite high and indeed, the share price whiplashed back around again. Total shareholder returns were almost 100% in the past year, which for a Canadian bank is absolutely ridiculous.

With the ship righted, a course charted, and engines on full steam ahead, and my nautical references exhausted, the bank has some exciting times ahead of it:

Valuation

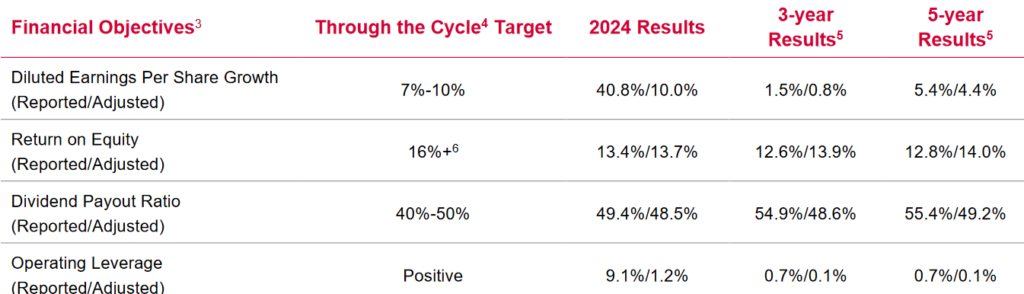

This brings us to the question of whether it’s trading at a fair price right now. As usual, I used Stock Unlock to complete my valuation. I used P/E as the valuation metric (10.5 5yr avg), assumed EPS growth on the low end of guidance (7%), and dividend growth slightly below this (5%) as I feel the next two years may pose a challenge to the bank with a significant amount of mortgages up for renewal so management may want to preserve some earnings to build capital to buffer against any losses. I also assume they don’t use their authorized share buyback and so stick with ~1% p.a. average share issuance.

Taken together, the FV is about $73/sh or almost 5% CAGR.

Increasing growth to the high end of 10% gets us to $82/sh or almost 7% CAGR.

If they can keep that growth, I think it’s more likely they would maintain their premium (to their average) PE. Right now the PE is over 13, but I use 12, resulting in a FV of $91.50 and just over 9% CAGR.

Seems like that’s what the market is pricing in, but for me it’s rich at current prices. I like the story, I like the direction, and I like the dividends (up another ~8% this year – a nice raise!), but I’m not going to add to this position right now.

*Perhaps apocryphal, but apparently the banks agreed to do this to help accountants who were otherwise busy from January-April with those whose fiscal year ends matched the calendar (link: https://archive.is/EI4k7)