Introduction

Texas Instruments (Ticker: TXN) is one of the largest manufacturers of analog and embedded chips. Analog chips process real world signals into something usable in the digital world. Think sound, temperature, pressure and light. They are cheap to make, but once customers choose a chip for their product they don’t tend to change them. Embedded chips sense, control, connect and process data. Think industrial robots, automotive sensors, appliances.

TXN enjoyed a pandemic-fuelled boom, but after global supply chains and demand returned to normal levels, customers were flush with inventory and demand dropped off. Then automotive and industrial markets also fell, affected by high inflation and central banks’ responses by raising interest rates. TXN pivoted in the past decade to focus on these two markets, which now make up about 70% of its business, and so it is keenly feeling the cyclical downturn.

Nevertheless, the long-term outlook is favourable, driven by rising demand for both existing and novel / new applications. TXN has also undertaken a large counter-cyclical investment to build out its manufacturing capabilities while taking advantage of attractive funding under the US CHIPS Act. With this coming to an end, the stock trading down about 20% off all time highs and approaching 52-week lows, and some interest from a fellow investor, I decided to review my valuation.

Situation Overview

I’ve owned TXN for almost a decade. Over this time, initial purchases have returned some 3x or almost 12% CAGR. The position has grown to about 15% of my portfolio, and it’s one I’m comfortable growing, due to the importance of its product in so many applications; its focus on quality and bringing manufacturing in-house; and management’s guiding principle of growing free cash flow per share.

This is front and centre of their investor relations page: “The best measure to judge a company’s performance over time is growth of free cash flow per share, and we believe that’s what drives long-term value for our owners.” quoting Rich Templeton, Chairman and former CEO who oversaw operations from 2004 to 2023 when COO Haviv Ilan took over. Templeton was fundamental to creating the TXN of today.

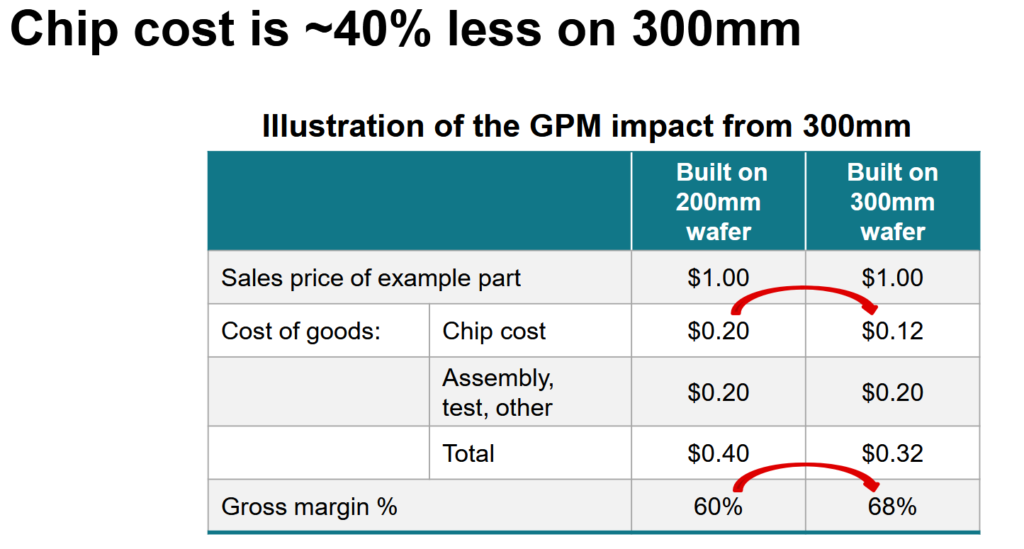

Templeton oversaw a period of significant FCF growth, enabled by TXN manufacturing chips on a 300mm wafer instead of 200mm wafer. This larger wafer enables a 40% cost improvement that drops to gross margin, and produces 2.3x more chips per wafer:

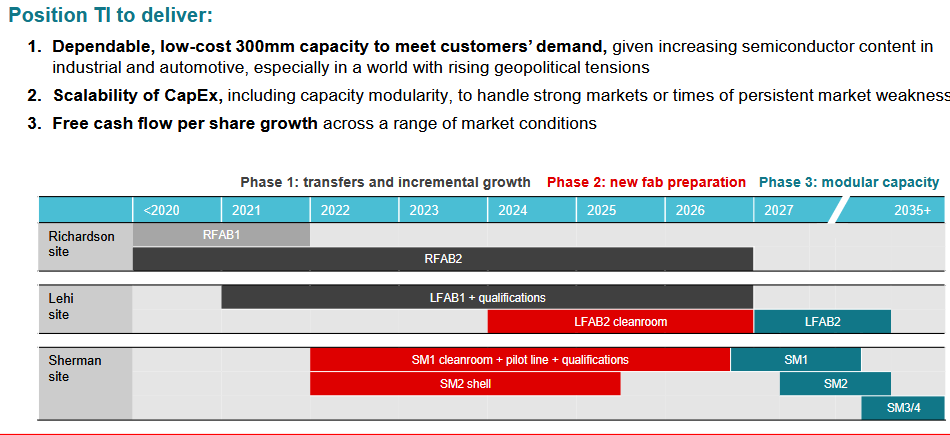

This shift was coupled with a counter-cyclical investment in capacity in the early 2000s, which was built in a modular way to better match investment with demand. This facility was RFAB1, and it sat unused for nearly 5 years. Then TXN bought equipment from a bankrupt competitor for pennies on the $ during the financial crisis, enabling it to complete RFAB1 cheaply and match investment with demand, which by 2010 had started to grow again.

This all stopped after the pandemic, however and the stock has underperformed as a result.

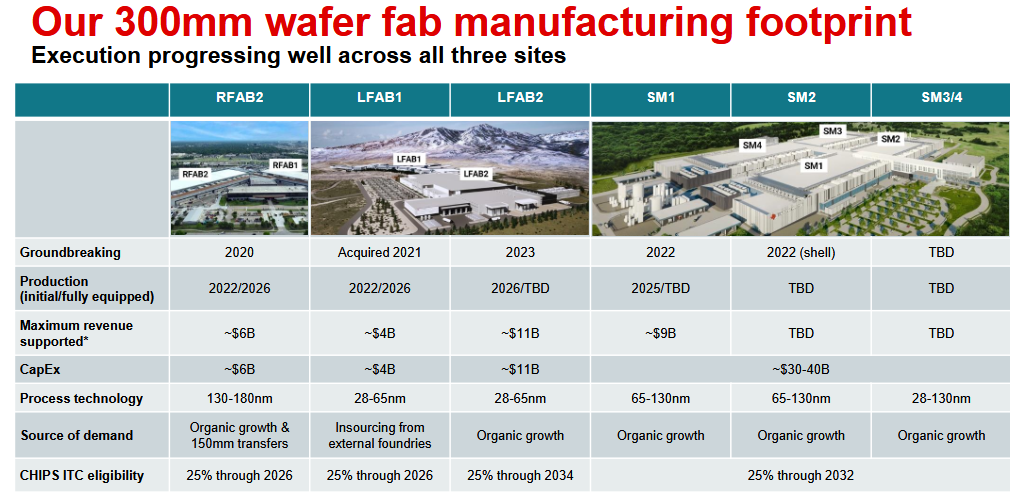

In 2022, management announced a huge counter-cyclical investment to build out their own chip manufacturing sites in the US, known as “Fabs”. Specifically, they would build 6 new 300mm fabs, spending $5B/year through 2026 and slightly less through 2030 to almost triple capacity by 2030. This is a staggering amount of money and was couched as intending to bring in-house more fab capacity, make more on the 300mm wafer, bring more capacity into geopolitically desirable control (TXN controls almost 50% of non-China+Taiwan semiconductor capacity), and to a lesser extent, take advantage of attractive CHIPS Act funding (direct cash + investment tax credits) to position the company to dominate over the next 10-15 years by having the capacity to meet demand at a level far exceeding any other semiconductor company.

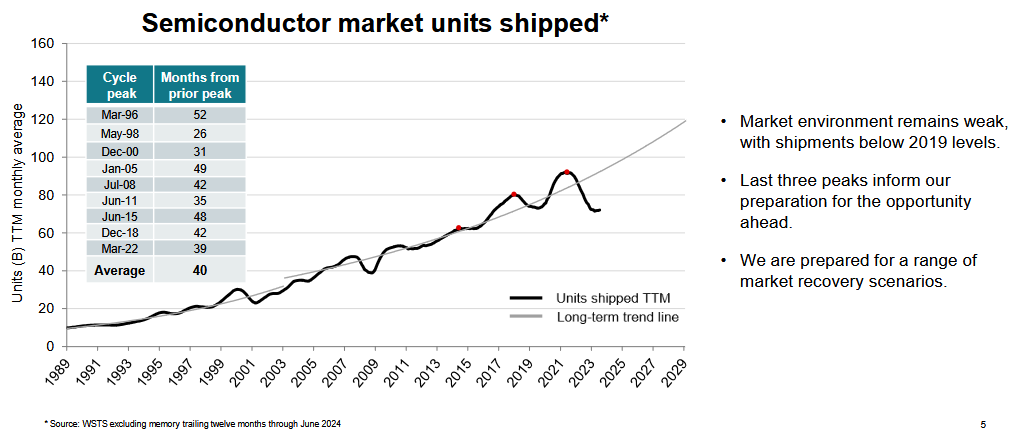

Sure sounds good, especially as TXN has lost market share throughout and after the pandemic. The problem is, the industry is in the deepest and longest cyclical troughs ever experienced, and long-term demand expectations suggest TXN’s capacity would exceed this by a staggering 50%!

Recent results also show that current management have eschewed the longstanding focus on FCF/share, despite regularly extolling this as their guiding principle.

Stock Unlock: TXN Stock Details – Cash Flow

I was admittedly concerned about these dynamics as the share price lagged peers, but willing to see through the fab investment on a long-term lens.

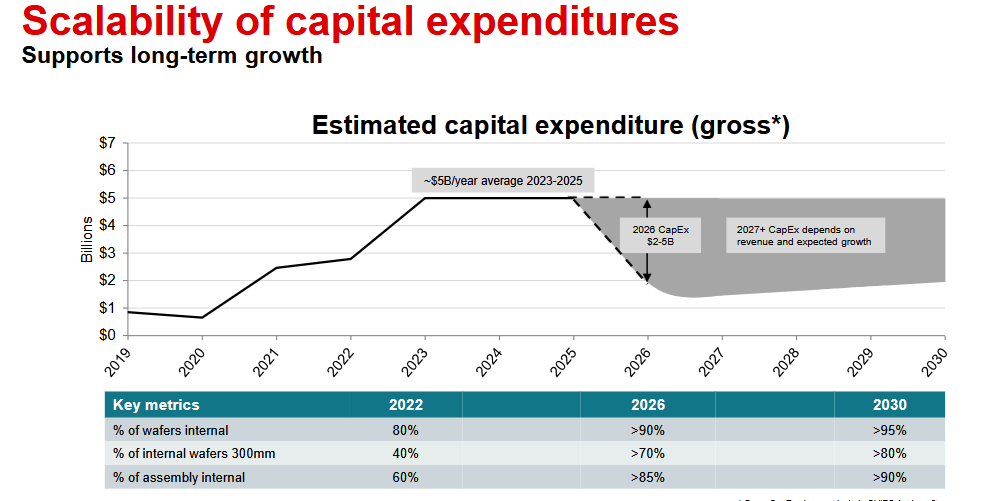

I wasn’t going to add to my position, however, simply due to how much was being invested. These dynamics also led to Elliott Investment Management to take a $2.5B stake in May/24 and agitate the board to make changes. They respected TXN’s history, position as the industry leader in capacity, margins and historic returns, but were disappointed by the lack of clarity of when FCF/share growth would be back on the menu, as well as the more recent weak stock performance versus peers. The letter signatories included Jesse Cohn, apparently one that CEO’s never want to see on correspondence. Elliott asked, and got, the following: 1) reduce overall capex spend and adjust remaining investments to be flexibly responsive to additional demand by partially completing some of the fabs, and 2) return to the company’s legacy of growing FCF/share.

Time will tell, but for now I see myself aligned with Elliott’s intentions and am happy someone with more heft could make an impact.

The revised approach is now clearly articulated in recent quarters’ investor presentation:

Implications for Valuation?

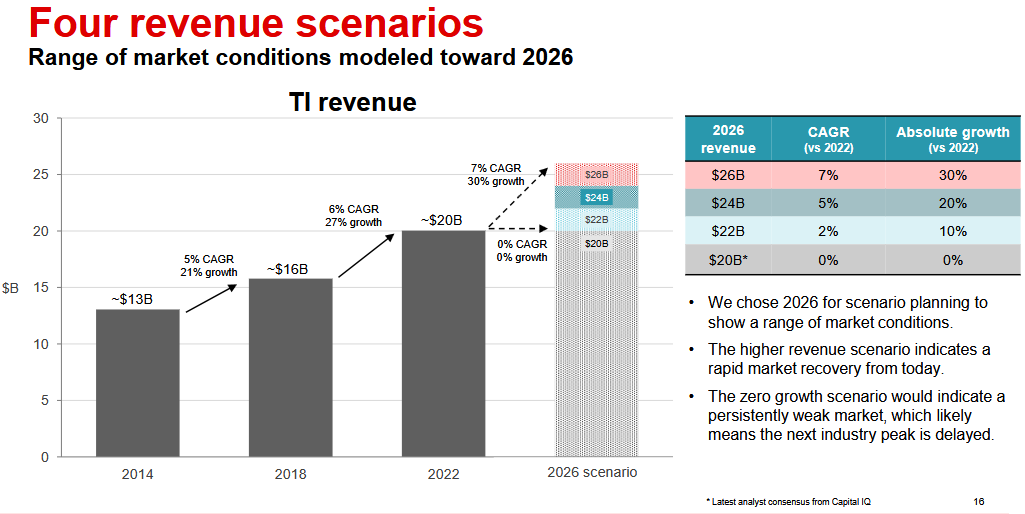

I started with their latest guidance for 2026, which covers four scenarios for growth between 2022 and 2026,ranging from no growth to 7% CAGR / 30% growth:

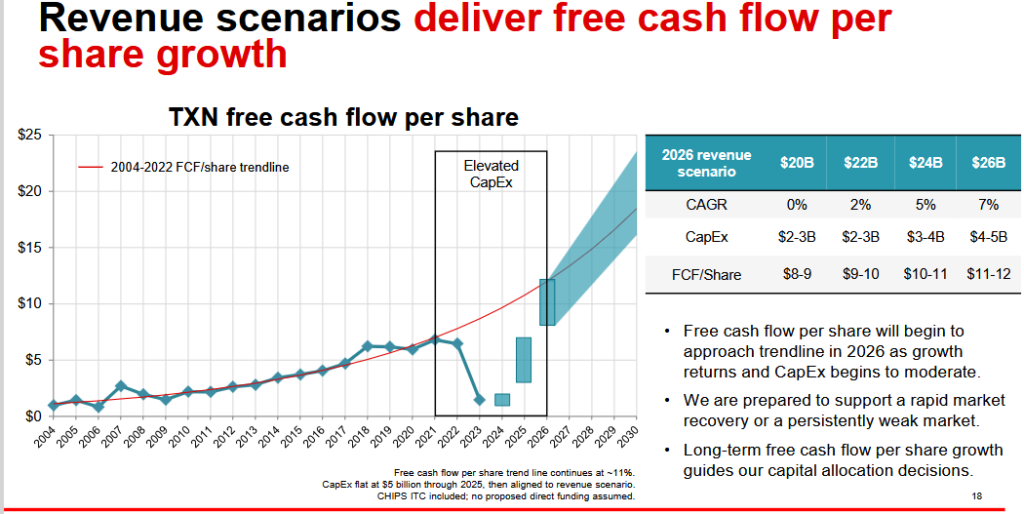

What I found intriguing is even in the no-growth scenario, FCF/share is estimated to be $8-9, with flexibility to meet demand if it’s higher than expected which is why capex is higher in those scenarios. Right now, FCF/share is $1.65 for 2024.

Alright, so a 5x in FCF in 2 years sounds pretty damn good, even if that’s a reduction in spending as opposed to business growth. I don’t think this point was overlooked and everyone should be aware of this though, since its so well telegraphed by the company. Plus I’m interested in a valuation over a longer-term, so I decided to look at a low growth case over 5 years from 2024 through 2029.

I assumed an average FCF/sh of $8.5 in the no-growth scenario, the midpoint, which is $7.8B by 2026 based on 912MM shares outstanding today (for simplicity I’m ignoring buybacks). I then assume that due to this type of environment growth is anemic at about 2.5% annually, which brings FCF to $8.3B by 2029, for a 2024-29 CAGR of 41%.

Management guided that all FCF will be returned to shareholders. With about $5.50/sh paid out now as dividends and assuming 5% growth annually through 2026, deducting dividends from the FCF leaves about $2.75/sh available for buybacks by 2026 or about 1.5% of all-time high share price. Similar to what they are buying back now.

The FCF multiple is about 54x right now, owing to the depressed level of FCF. It’s also averaged 54x over the past 5 years, but this was a boom period. The 10-year average is about 37x and the median is 22x, so I cut the difference and assumed 30x.

This shows a potential 12% CAGR at current prices, with a FV of $202.5/sh for a 10% CAGR.

Stock Unlock: DCF Calculator

This obviously looks better if there is a boom, and there is further upside because it doesn’t include the $1.6B of direct funding under the CHIPS Act that will be received through 2030. This is another $1.75/sh of cash.

Ordinarily, I would use operating cash flow to value a company with a significant amount of investment resulting in variable or unreliable FCF. In this case, the company has guided pretty clearly what to expect in terms of FCF and supports using it for valuation.

Where Does This Leave Me?

I think we’re going to see a rising demand for TXN’s chips. As merely one example, EVs use 2-3x more analog chips than ICE vehicles. In the 1990s, average vehicle chip content was $30-50, and as of the 2020s, this has risen to $400-600 for ICE and $800-1500+ for EVs (or more for luxury or autonomous vehicles).

This doesn’t consider continued factory automation, replacing aging energy infrastructure, body electronics and lighting, autonomous driver systems (see continued AV investment by Uber, Waymo, and their ilk as an example), general/broad robotics, healthcare, and consumer products like AV/AR headsets being developed by META. Add on top of all this continued investment in AI and data centres, with associated requirements for electricity grid additions and new power generation, and the long term picture is attractive.

TXN is 70% through a massive investment program that will support the company for the next 10 to 15 years, with flexible capacity to respond to unanticipated market growth. Based on my FCF valuation, which assumes almost no growth, I’ll add to my position under $180/sh.