The reference to Retracked means to go over a prior section of rail track to make repairs or adjustments. This post is about me revising prior views.

Since I last wrote about CNR in August, the price has run up about 10% and floated back down to ~$155/sh. I’ve also listened to over three dozen hours of investing podcasts* and read several investing books.

Guy Spier happened to feature in quite a few of these. He runs the Aquamarine fund, which averaged 9% CAGR since inception. A solid, steady return. Not remarkable compared to Buffet or the Nomad Partnership, but it still beats the index and when that annual difference is compounded over decades, it makes a significant positive impact.

Listening to Guy and others, I came upon a concept that is a mix of probability and spirituality. I won’t do the explanation justice, but it’s along the lines of considering our decisions and life on a path of a 1000 possibilities, and making decisions that would result in a positive expected value in the majority of them. Put another way, in the context of investing, one might do really well with leverage – this time. In another possible life, it may ruin us. In a similar vein, always striving for huge returns may work out well, but it may lead us to taking larger risks that lead us to ruin (capital loss). It’s similar to what Annie Duke talks about in her books Quit and Thinking in Bets.

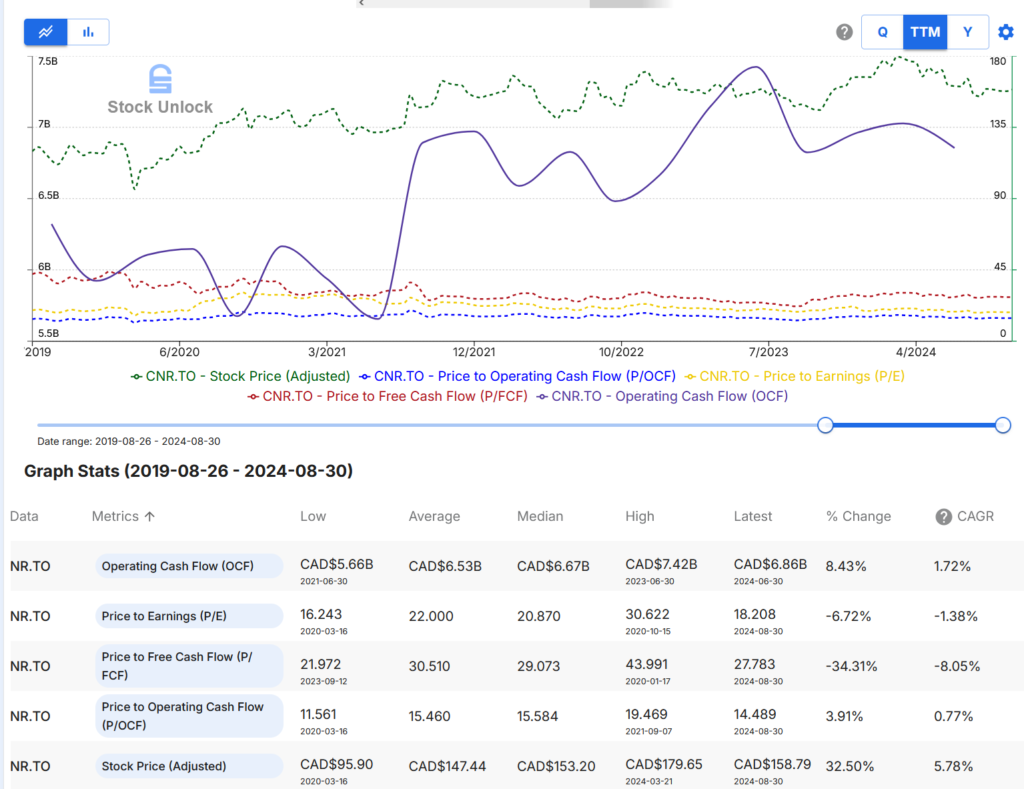

It made me reconsider the somewhat absolute statement I made when I evaluated CNR at a similar price to where it is now. Firstly, I said it wasn’t market beating, so I would avoid it. Specifically, that an 8-12% CAGR was insufficient. Secondly, I wrote the article after reading someone else’s post about CNR not being an attractive investment, clearly biasing my own views in the interest of publishing something provocative. Thirdly, when I calculated my own returns from CNR, I only considered the share price appreciation of ~7.7% CAGR. I didn’t consider the dividends, which add another ~2% to that and bring total returns to nearly 10% CAGR.

I asked myself, knowing what I’ve learned in the past three months, what do I think now? Well, doubling my investment every 7 years? In a business I consider high quality and irreplaceable? That’s nothing to sneeze at. Can’t say I like the increasing leverage, partly to fund those big share buybacks, but I think it was partly in response to the Kansas City acquisition by CP in 2021 to give shareholders a reward of sorts. Even if I would have preferred them not to lever up. Having said that, their leverage target is 2.5x, which they are sitting roughly at now as a result, so it may have been merely taking advantage of spare borrowing capacity supported by their fairly robust underlying business results. It’s something I’m going to keep an eye in any case.

In my prior article, I also thought it was not realistic to assume current multiples would expand back to historic levels. That’s a reasonably safe assumption, insofar as then any expansion is “gravy” if the price one buys at is sufficiently attractive such that returns don’t rely on expansion. That hasn’t changed.

What I didn’t consider, however, was another source of returns: share buybacks. CNR buys about 1-2% of shares annually and reduced its share count by 2.5% CAGR over the past decade.

As I thought more about CNR, I considered the three engines of value: earnings, multiple expansion, and share buybacks. Thanks to John Huber of Saber Capital Management for this framework (link). [Note – I think he misses dividends, so I consider them alongside share buybacks in a ‘shareholder capital return’ bucket].

All this to say, I reconsidered my earlier posture against CNR and have come to the conclusion that at these prices, it is compelling as a solid base to my portfolio. Am I fairly certain about this outcome? Yes. Arguably, I should overweight my investment in it, as compared to a more speculative position.

It’s about positioning to win in the long-term, in the greatest number of possible paths my life might take me.

And why not? This track record (pun intended?) is enviable:

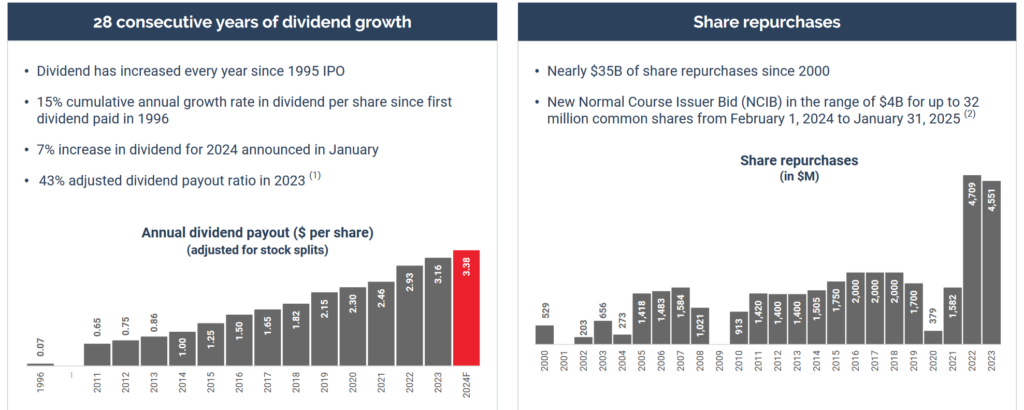

Based on the Q3 guidance for 7% dividend growth, high single digit EPS growth for 3 years, and assuming 1% buyback annually with the P/E unchanged at ~18x presently, the CAGR is 9.5-11.5% based on 6%/8% EPS CAGR. Add a mere 2x increase in the multiple closer to historic average of 20x, we’re looking at 13-15%. The way CNR intends to grow at this GDP+ rate is through own initiatives. These include: i) Expanding at the ports of Vancouver, Prince Rupert, and possibly Montreal, Halifax and St. John, ii) taking advantage of their owned bypass rail around Chicago (speeding up transit times up to 48hrs faster than those who have to go thru the city), iii) introducing automation e.g. Autonomous track inspection cars that run in regular routes, autonomous inspection portals, and handheld tech for field staff, and iv) implementing and sticking to scheduled railroading, which enables them to quickly recover after incidents (like the stoppage due to the fire in Jasper). From the 2023 investor day, as reported in Progressive Railroading (which is not PBR nor focused on making the longest possible trains):

“The way this model works on our railroad is that the plan is created at the center. [It] looks at all the volume across the network and all the parameters,” said CN President and CEO Tracy Robinson during investor day.

Then, a plan is crafted that can optimize the entire network instead of meeting the operating needs of individual yards and facilities. And the plan is the plan — there is no backup or alternative.

I admit it seems contradictory to write a different position on the same stock a mere three months later, but I’ve learned a lot in this intervening period. Plus, the whole point of committing my thoughts to (virtual) paper is to record my thinking process, and that evolution over time. This reminds me of John Maynard Keynes – “When the facts change, I change my mind. What do you do, sir?”

Consequently, I bought some more shares around $154.

* The combination of a long commute and training myself to listen at 2x speed means I can devour audio. Another example of the power of compounding. Try it out.