Overview

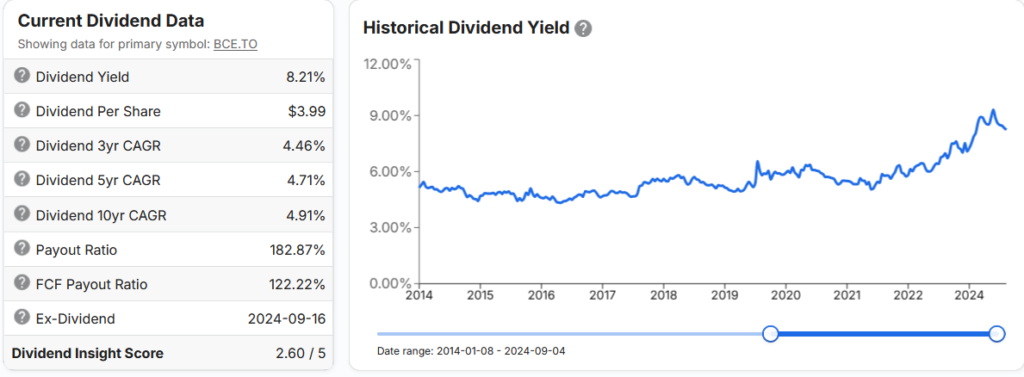

With some interest in dividend circles over BCE’s seemingly juicy dividend yield of 8.2% (as of Sep 5/24), I decided to review my thoughts nearly a year on from selling this former core part of my portfolio. I first bought BCE in January 2015 for $53. I sold it in November 2023, almost 9 years later for…drum roll, please…$53.85. Including dividends, my CAGR was a measly 2.7%. According to the Bank of Canada, inflation also averaged 2.7% over this period, so I earned 0% in real terms. So much for safe.

Setting the Context

BCE has long been a favourite for income investors, with a steady yield and growing dividend. It’s why I originally bought it, when I was looking for good, safe, dividends. Which it certainly paid out, but really only ever done that:

Stock Unlock: Dividends for BCE 2014-2024/09/04 (pulled Sep’24)

BCE did provide a stable yield, but this came with very low price growth (<5% CAGR) and frankly sub-par returns. I recognize that I say this with the benefit of hindsight. With my value lens now, would I have done differently? I wish I could say I would have sold around $70, but I really don’t know.

Peering into the Behemoth that is BCE

It was an exciting time in the late 2010s. Operations were generating ROIC around 15%, wireless subscriber count was rising, Samsung and Apple constantly rolled out phones, FCF was ticking up and all seemed well in hand. Bell even managed to close the acquisition of MTS in early 2017, and started embarking on a huge build out of a national fiber optic network to leapfrog Telus and Rogers by providing fiber-to-the-home and a backbone of the new national 5G wireless network.

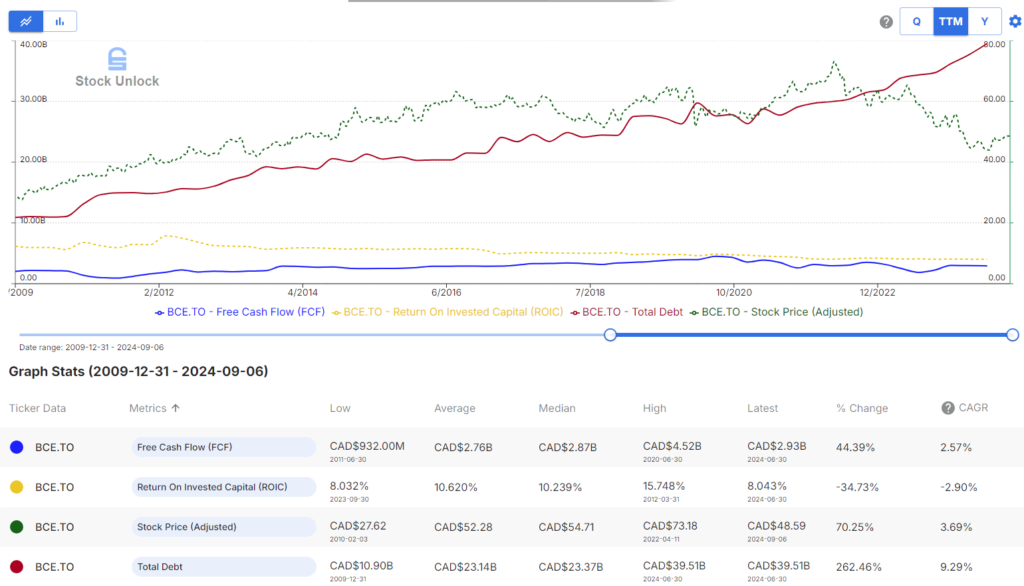

All this cost money, and a lot of it. Looking over my notes, I picked up on cracks in 2021, after reading that they spent a whopping $7B on capex. Coupled with a portion of their legacy high margin business starting to run off, competition with Telus and Rogers, something had to give. They simply weren’t growing and more than doubled their debt pile since 2010:

Stock Unlock: Financials for BCE, summary income statement 2017-2023 (pulled Sep’24)

Stock Unlock: Free Form for BCE, Share Price, FCF, ROIC and Total Debt 2010-2024/09/06 (pulled Sep’24)

With the share price tumbling, a growing debt pile, anemic growth, and noise over regulation, I decided to pull the trigger and sell out in the Autumn of 2023. It was a difficult decision for a formerly income-focused investor. The fundamental part of me couldn’t rationalize holding it any longer though, especially once it reached the point that they could no longer generate FCF to cover their dividends. That set off alarm bells.

It’s Not Me Darling; It’s You.

My unease wasn’t something I woke up with, but something that grew since about 2020. Management struck me less as stewards of their shareholders’ capital and more interested in their own rewards. They chose to continue to raise the dividend, which wasn’t necessary, instead of taking a harder decision to preserve the company for a long-term benefit. I read that 2023 marked 16th consecutive year of dividend growth. Sounds good, until one realizes that by year-end 2023 they needed to borrow to pay dividends to the tune of at least $600M per year, rising to $900M based on LTM Q2/24. As a result, BCE is creaking under the weight of its debt and recently had its credit rating downgraded to one level above ‘junk’ status.

Management also blamed government regulation for the decision to cut back on investment by $1B over 2024-25. Specifically, they cited having to grant access to their network to wholesalers in Ontario and Quebec. These players may present competition and BCE does not want that. It may be true, but I also think their excuse is disingenuous, and that pointing to regulation was a smokescreen. Using it as a convenient excuse, it enabled them to save face and not have to take accountability for their investment decisions and poor results. As an aside, there is a reason why the UK forced British Telecom to separate the network infrastructure from the retail/service part of the business, into a legally separate entity called Open Reach (link).

These are only two examples of management actions that I disliked (I realize the capex cut came after my sale, but it was being considered ahead of that while I was still a shareholder). Two more examples are:

- Taking advantage of corporate welfare to avail itself of some ~$150M of COVID-era funds from the Government of Canada in 2020. BCE did not need this given it’s (then) sufficient FCF, access to the debt capital markets, and drawing over $1B on its revolver during 2020 as a cash backup which it subsequently repaid. Management even admitted, in the public furore that followed the revelation of large Canadian companies taking advantage of CEWS, that the amount of money was immaterial.

- Corporate decisions that ran fiber to the CEO’s cottage, while leaving other year-round residents lacking (link).

Of course I don’t believe the CEO is responsible for making every decision, but they are certainly responsible for decisions made in the enterprise. The sum of these actions suggest a corporate culture that I don’t agree with and turned me off the management team.

“In the Long Run, the Market is a Weighing Machine”

It’s fair if one wanted to leave qualitative assessments aside, and look at some numbers instead. I already pointed out above that growth stalled, debt grew, and was further exacerbated by having to borrow more to pay the dividend. Operations were also generating worse returns over this time:

Stock Unlock: Financials/Metrics for BCE (2013-2023)

Taken together, they had underwhelming stock market performance, even well before the Pandemic. This merely continued post-Pandemic, once the euphoria wore off:

Stock Unlock: Returns detail for BCE (2014-Sep’24)

Concluding Remarks / Actions

I don’t think they will go under, but I think it will take years to clean up their capital stack. All the while I don’t expect their stock price will do much, there won’t be as much cash to invest in the business, employees and customers may suffer (even more) cost cutting efforts, and dividends being cut is a very real possibility.

Clearly, there are much better places to put one’s money, whether for income or for growth. This review confirms my decision to get out of this position. I merely wish I had started writing my thesis for each investment sooner (hence part of this blog reviewing each position I have). Had I done this, I’d like to think I would have been in a better position to decide to sell sooner, perhaps with a modest gain. Perhaps not. I haven’t really lost money, just the time this investment could be put elsewhere.

The lesson here I suppose isn’t necessarily that dividend investing is bad, but not having a reason to invest in a company beyond income isn’t inherently prudent, and there is an opportunity cost. I would have done better with almost any other of my investments over this time period.