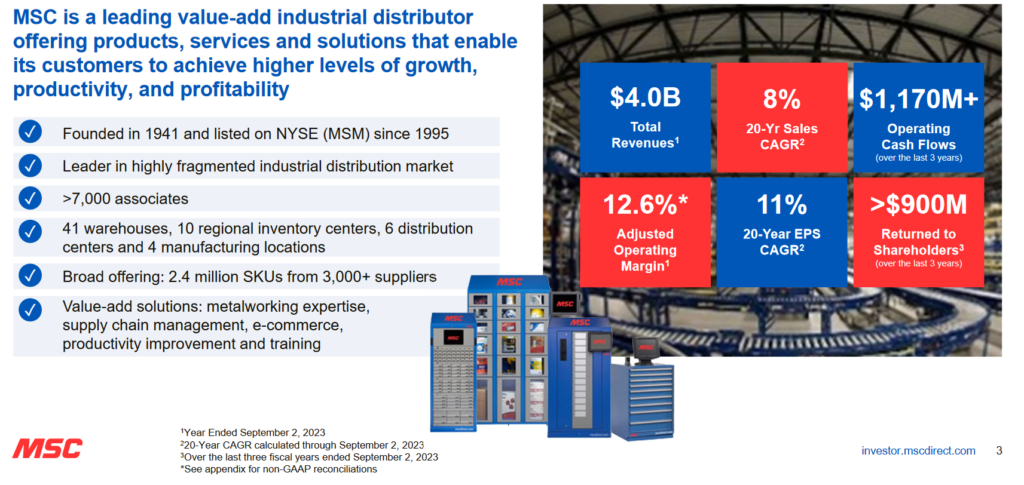

Business Overview

MSC Industrial Direct (ticker: MSM) is a distributor to light and heavy industrial customers, with a niche in specialty metalworking. They source products and maintain inventory for their customers. These include fasteners, cutting tools, safety equipment, welding supplies, and electrical supplies, among other products. It started as a cutting tool marketer in 1941, Sid Tool, Inc., founded by Sidney Jacobson. It acquired the Manhattan Supply Company in 1970, and then changed the name to MSC Industrial Direct. It IPO’d in 1995.

Customers & Competition

Customers span government, MRO, Fortune 1000 companies and individual machine shops.

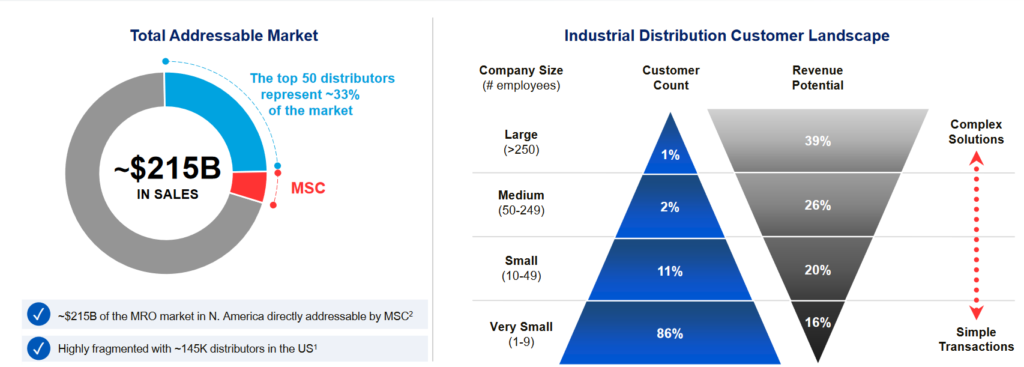

Distribution is a very large, and highly fragmented, market. MSC estimates their TAM is $215B, as compared to their 2023 revenues of $4B, and the top 50 distributors represent approx. 1/3 of that market.

In this, there are 19.5MM potential customers and MSC can serve the 750k metalworking customers.

Despite growing at 10%+ CAGR for years, which is greater than their underlying market and means they are gaining market share, they have a small share of the overall market. This is comforting to me insofar as there is a large runway to grow and no dominant player to sweep smaller companies aside.

Notes on Operations

Beyond product distribution, MSC provides inventory management and supply chain solutions, leveraging its “deep expertise from more than 80 years of working with customers across industries.” (2023 annual report).

A significant portion of revenues, 60-70%, come from manufacturing, and about 45% of sales has to do with metalworking This exposes MSC to cyclicality, but this specialization in metalworking is also a differentiator within the broader MRO market.

They guarantee same-day delivery, with 99% of SKUs held in stock. This was unique before the advent of the internet, but still remains a differentiator.

In addition to shipping, they operate on customers’ premises with vending machines and what they call in-plant locations (aka Onsite if one is reading across to Fastenal). They are trying to shift from being a spot buy supplier to a partner, and is earlier on their on-premises journey than Fastenal. It may mean large accounts have greater purchasing power and push down MSC sales prices, but higher volumes and switching costs should come with that shift and mitigate lower prices.

In addition to being a supplier, they provide technical expertise, inventory management, and productivity improvement programs, to capture a greater share of their customers’ overall spend.

They seem to use a mix of owned and leased premises. I prefer owned premises because it gives more optionality and potential hidden value, than a leased one where you are at the whim of a landlord that needs to make a return on their real estate. Specifically, they own five of their 6 fulfilment centres, but lease operational locations. It seems more of a balance, owning what is more critical.

Observations from Investor Days & Recent Developments

Major control block held by founding family

The founding Jacobson/Gershwind family still controls MSC, and the grandson Erik Gershwind is the CEO. His uncle, Mitchell Jacobson, is the former CEO and current non-executive chairman. Erik’s mother, Marjorie, is Mitchell’s sister.

In 2023, they simplified the capital structure by collapsing the class B super-voting shares that the founding family owned. Now, all shareholders own the same class A shares. The founding family’s economic interest is 21%. They also voluntarily agreed to limit their voting to 15% of shares outstanding. Any shares they own in excess of this will be voted pro rata with votes of unaffiliated class A shareholders. Another independent director was added to the board and they completed share repurchases in fiscal 2024 to offset dilution.

Lagging peers in e-commerce solutions

The industry trend is for customers to purchase online – e-commerce, in addition to vending – but MSC has been slow to address this change. As a % of net sales, it’s been flat around 60% since 2017. Management only recently started to address this in 2024, and it’s been a troubled roll out that is thankfully nearing the end. They’ve been upfront about this in analyst calls, and expect the investment to be complete by Q1/25, after which they will launch a marketing campaign to bring awareness to the changes.

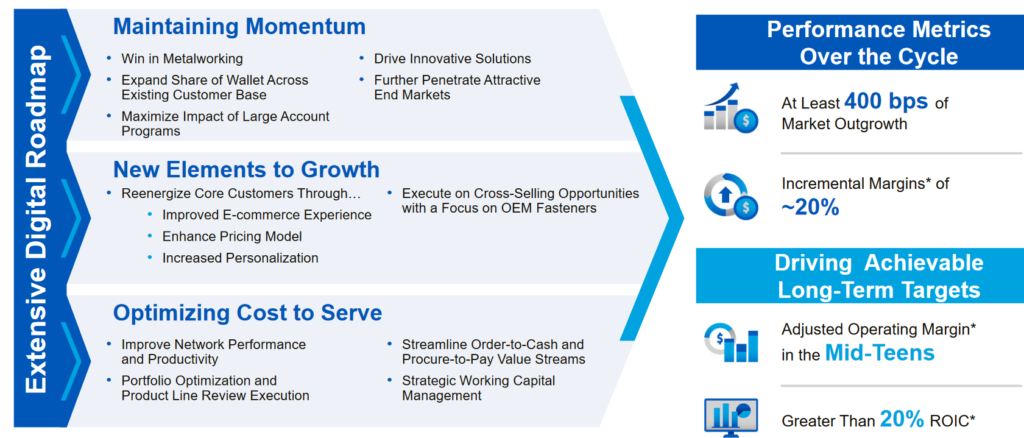

Mission Critical

In 2020, they launched the “Mission Critical” program to accelerate market share capture and improve profitability. This includes expanding its metalworking specialist team, expanding solutions (e.g. on premises vending), enhancing e-comm, diversifying customer base and end markets including government and national accounts. The initial phase concluded in 2023 and now they are in what is described as “Phase 2”: maintaining momentum by continuing to invest in what I just described; re-energizing the core customer base (pricing, personalization, cross-selling), and optimizing their cost-to-serve. Long-term targets are:

- At least 400bps of growth above market

- Incremental margins of 20%

- Adjusted operating margin in the mid-teens

- ROIC >20%.

Management Review & Compensation

I like the balance between genders on the board. Diversity of thought and experience is important in a fast evolving world.

The CEO, since 2013, is Erik Gershwind, the grandson of the founder. He started with MSC in 2005, working in various roles.

The CFO Kristen Actis-Grande joined in 2020, after nearly 2 decades with Ingersoll Rand, running the finance department for various business lines.

Call out to Martina McIsaac, the president and COO, which is unusual in an American company (usually the CEO/President/Chairman is wrapped in one role). She joined after a decade with multinational Hilti, ending as region head for N. Am operations, and about 15 years with Avery Dennison. I like that she has international experience, and experience in large organizations.

Interesting that Brian Bello, is interim CIO as of Jun/24. He’s been with the company since 2008 and I think he’s going to be in the hot seat for sorting out the issues with MSC’s e-comm roll out. He has a background as a consultant, which I don’t like, but he does have both computer science and math degrees.

Compensation is a combination of 1) base salary, 2) short-term incentives based on organic revenue, adjusted operating margin, and individual goals, and 3) long-term incentives based on annual average adjusted ROIC, measured over 3 years and cliff vesting after 3 years, or shares vesting over four years (equally).

Their short-term incentives only paid out 55% of bonus targets for 2023. They clearly are paying to retain, but not paying when they don’t perform. I’m ok with this, especially with ROIC being the driver of the cliff-vesting incentives and shares vesting over a longer period.

Financial Review

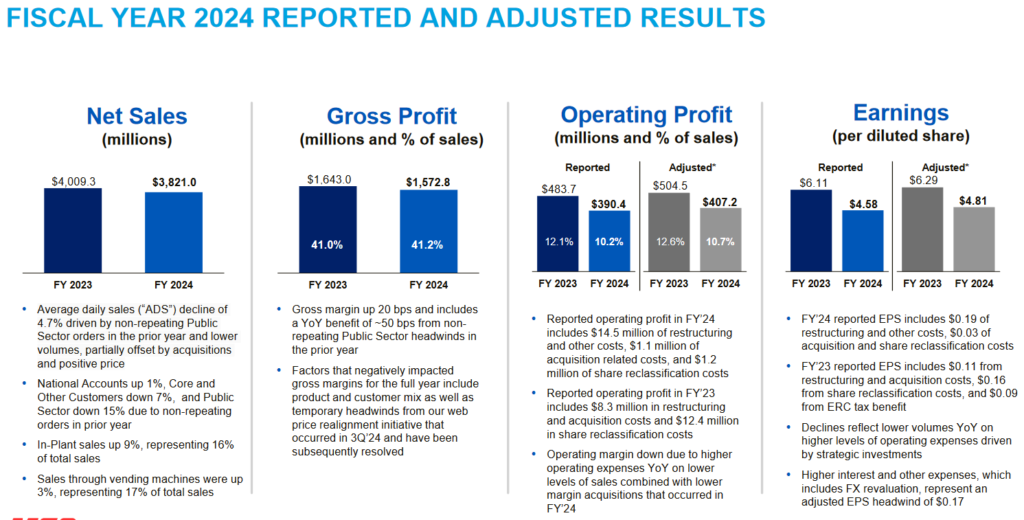

2024 just wrapped up – their fiscal year end is Aug 31 – and it was a challenging year. MSC’s primary end markets are metalworking and heavy manufacturing, and both sectors had weak demand. Adding to weak demand is the troubled rollout of their new e-commerce platform. This involved significant upgrades in the back and front ends. The issue for MSC, or rather their customers, had to do with pricing and some technical issues.

Sales for the year were impacted by the loss of non-repeating public sector orders (3% of the 8% drop) and lower volumes (5% of the 8% drop) due to weak sector demand. Only 34 of their top 100 customers showed growth.

Vending is a bright spot, flat y/y and representing 17% of net total sales. Their implant programs were up 5% y/y and these are 16% o total sales. Gross margin outperformed historic seasonality and was up 0.5% y/y, helped by the team’s response to the hampered rollout of e-commerce pricing.

Net debt is low, at 1x EBITDA and <30% of the balance sheet. Working capital had a favourable impact on cash flow. I was worried if their customers were taking longer to pay and/or inventory was building, but this doesn’t appear to be the case. Cash conversion was 160% for the year, above the 125% target.

I like that they intend to provide a longer-term outlook as the environment in fiscal 2025 stabilizes; for now they are going to stick with quarterly. Right now, it’s not pretty, with the expectation that sales will be down again by ~5%. The US election isn’t helping, because customers are holding off on purchases, but that’s temporary.

The issues are central to management’s focus and it seems this has been fixed, or at least ameliorating, with gross margin increasing in Q4.

Sales weakness has been offset by support from their ‘high-touch’ activities, including sales from vending machines up 9% and in-plant programs up 29%. Despite lower volumes, there are more installations, showing that operating on customers’ premises can be a counter-cyclical source of growth. They also bought back ~2MM shares during the year, or nearly 4% of shares outstanding, but that is really only offsetting the dilution impact of the share simplification last year; nevertheless, it’s a start.

Capital Allocation

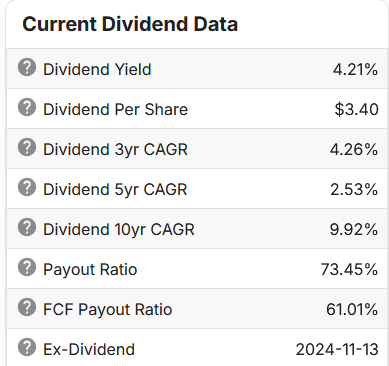

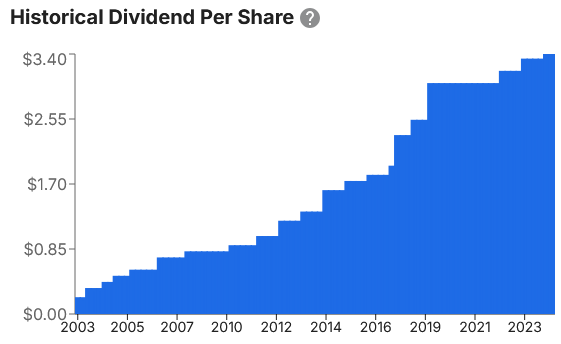

MSC started paying a dividend in 2003, and it has regularly increased but the pace of this slowed in recent years. Payout looks high right now, because earnings and FCF took a hit in 2024. It’s still well covered and historic levels are in the range of ~50% FCF and 50-60% of earnings.

|  |

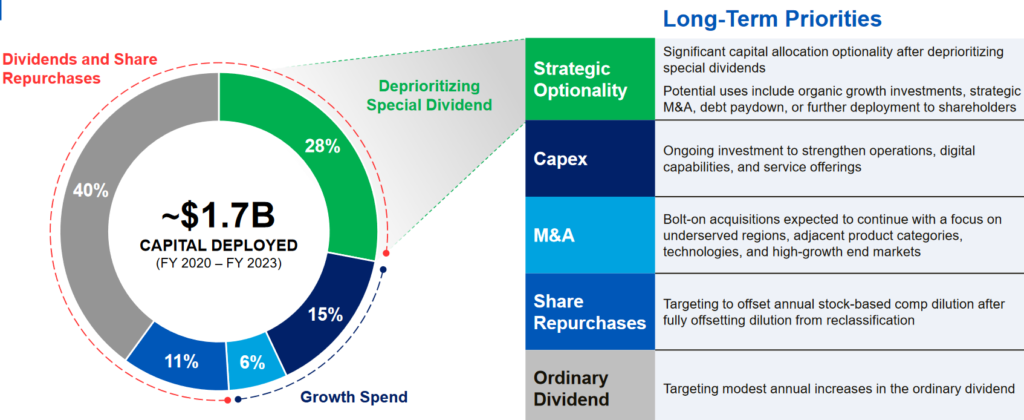

They also paid special dividends in 2015 and 2020, but after shareholder complaints about it being unreliable this was de-prioritized. The board intends to use this excess capital for a combination of organic growth, share repurchases and tuck-in acquisitions. This makes sense to me, given how fragmented the market is. It is also consistent with their history of M&A e.g. CCSG in 2015, DECO in 2017, AIS in 2018, Buckeye Industrial and Tru-Edge in 2023, and four more in 2024 (Canadian metalworker KAR industrial for $8.3M; Wisconsin metalworker ApTex for $5.6M; Arizona carbide cutting tool manufacturer Premier Tool Grinding for $10.6M; and IP from SMRT to enhance tech capabilities).

After reading investor material and Q&A during their fiscal 2024, I pieced together the following acquisition criteria:

- ROIC is the key metric used to evaluate a target. It should generate returns > WACC within 3 years.

- The acquisition should enhance market share and add valuable talent.

- Accretive to earnings within the first year.

- Focus on tuck-in acquisitions, which minimizes integration risks.

- Expect to drive synergies to improve margin to MSC levels (cost and/or operational)

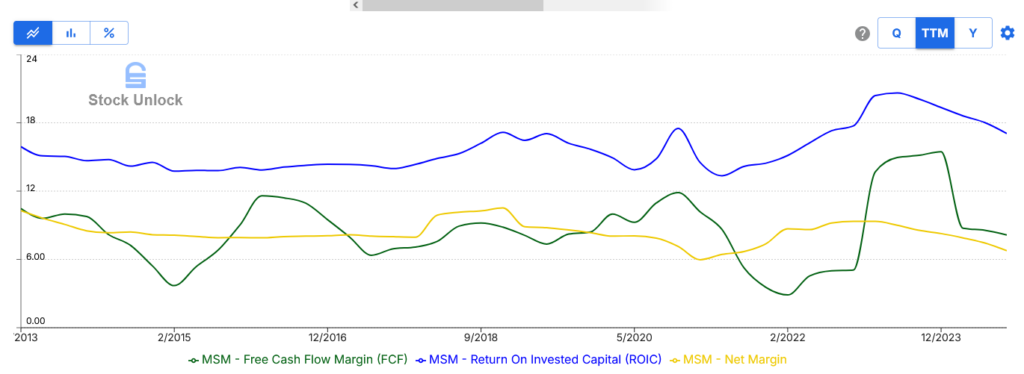

Returns on their activities are attractive, hovering in the high teens for over 10 years. I also like their margins for an industrial company. One can see the impact to their margins the destocking after the pandemic and their troubled ecommerce rolling in 2024 have had.

Stock Unlock: Free Form tool showing FCF, ROIC and net margin 2013-2024 (retrieved Nov’24)

Valuation

This isn’t straightforward to value, and there is no guidance of note to work with. I also am not keen on any complicated analysis. Assuming they manage to just get back to previous high earnings of about $350MM p.a. (achieved in 2018 and 2023) with no share count growth and average p/e multiple of 18x gives a ~9% CAGR at current prices over 5 years with a FV of $84/sh*.

Assuming they buy-back ~1% of shares per year brings this to 10% CAGR and a FV of almost $88/sh, and if the issues are fixed, margins increase as they set out to do (20% increase) and multiple expands 10% to 20x, brings this to a 13% CAGR and FV of $101/sh.

*Note that FV is based on a 10% hurdle rate.

Conclusion

I found MSC after a discussion on the Stock Unlock Discord channel, in response to my post on Fastenal. It was suggested that I look into competitors because Fastenal was expensive. WW Grainger is one, which I found both pricey and not at all unique because of how much various product it distributed. I think it opens it for more competition from Amazon business. While MSC may not be immune to Amazon Business, it is in a niche that requires high grade equipment for metalworking, which I don’t envision a tool shop buying on the cheap.

I also couldn’t believe the market reaction to Fastenal’s Q3 results. They beat expectations by a penny, both revenue and EPS, and the price jumped 10%. It’s even more expensive now. Sometimes, the market doesn’t make sense and I’ll continue to wait that one out.

In the meantime, I find MSC is in an interesting position. They are trading at 2015 prices, but their per share metrics are much higher. There’s a reason for it, they’ve been late to move big into e-commerce vs. Competitors, which they have been called out for and management acknowledged. The Q&A in some of the earnings calls struck me as being transparent about the issues, and what they are doing to address it.

Their business has very strong cash conversion, 100-125%+ of net earnings! Add a well capitalized balance sheet, high ROIC, and a plan to improve, makes this an interesting play. I also believe that long-term re-shoring of manufacturing, especially under a Trump administration, could help here, plus infrastructure investment which will require heavy manufacturing.

My take is that this company is in a turnaround of sorts, with cyclical weak end markets. I decided that I’m not going to buy a stock that I’m not willing to hold at least two years, and this definitely fits that time horizon if not longer.

I don’t expect it will be a smooth earnings recovery in reality, as suggested by the valuation analysis, given that I believe 2025 will be another weak year before some recovery beginning in 2026 and beyond. In the short-term, catalysts I will keep an eye on their comments around completing the website overhaul and the marketing campaign associated with the launch. Then I’ll also watch for any tuck-in M&A that adds to growth. Long-term catalysts to watch for will be how they perform against “Mission Critical” phase 2, and end market activity (heavy industrial, metalworking).

I bought a starting position before Q4 results around $80/sh, results were weak, shares dipped about 5% in response but mostly recovered. I added some more around $79. I couldn’t make heads nor tails of why shares dropped, there wasn’t anything new except perhaps the market didn’t like the downbeat comments on guidance for next year. Maybe? I don’t really know and won’t begin to pretend to be able to predict price movements. Suffice to say I wasn’t surprised by anything in the results.

For this recovery play, I can wait. I’m buying at a 7% FCF and earnings yield around 6%, earning a 4%+ dividend yield with payout well covered by FCF, with management team that has a plan in place, isn’t shy to talk about their challenges, implemented some shareholder friendly changes to their ownership and include long-term metrics in their incentive comp, plus a strong balance sheet and history of FCF generation in all cycles.

I think there is something to it. Or maybe I’m just seeing what I want to see because I want to do something, and I’m merely impatient to wait and buy Fastenal at a cheaper price. After today’s jump in response to the US election, I’m already up 10% on my purchase, but the whole market seemed to like the election result. In reality, this is a slow burn investment and time will tell.

“Never let the future disturb you. You will meet it, if you have to, with the same weapons of reason which today arm you against the present.” —Marcus Aurelius

So with that said, when prices drop below $85 I’ll continue to top up, and will revisit the confidence in my valuation by tracking their performance against their goals as this develops in the next 18-24 months.